Page 9 - Working Paper (The Myths and Realities of Tax Performance Under Semi-Autonomous Revenue Authorities)

P. 9

DDTC Working Paper 0213

9

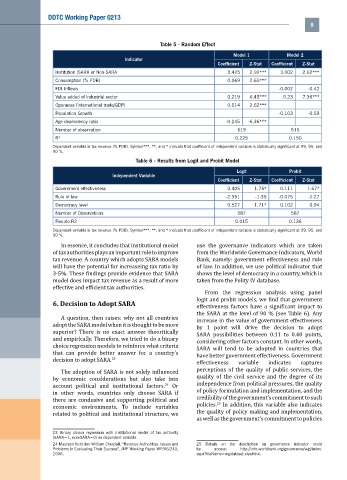

Table 5 - Random Effect

Model 1 Model 2

Indicator

Coefficient Z-Stat Coefficient Z-Stat

Institution (SARA or Non-SARA 3.425 2.92*** 3.002 2.62***

Consumption (% PDB) 0.069 2.65***

FDI Inflows -0.002 -0.42

Value added of industrial sector 0.219 6.45*** 0.23 7.36***

Openness (international trade/GDP) 0.014 2.62***

Population Growth -0.103 -0.59

Age dependency ratio -0.145 -6.36***

Number of observation 519 515

R 2 0.225 0.150

Dependent variable is tax revenue (% PDB). Symbol***, **, and * indicate that coefficient of independent variable is statistically significant at 99, 95, and

90 %.

Table 6 - Results from Logit and Probit Model

Logit Probit

Independent Variable

Coefficient Z-Stat Coefficient Z-Stat

Government effectiveness 0.405 1.75* 0.111 1.67*

Rule of law -2.951 -1.35 -0.075 -1.27

Democracy level 0.527 1.71* 0.102 0.94

Number of Observations 587 587

Pseudo R2 0.015 0.136

Dependent variable is tax revenue (% PDB). Symbol***, **, and * indicate that coefficient of independent variable is statistically significant at 99, 95, and

90 %.

In essence, it concludes that institutional model use the governance indicators which are taken

of tax authorities plays an important role to improve from the Worldwide Governance Indicators, World

tax revenue. A country which adopts SARA models Bank, namely: government effectiveness and rule

will have the potential for increaseing tax ratio by of law. In addition, we use political indicator that

3-5%. These findings provide evidence that SARA shows the level of democracy in a country, which is

model does impact tax revenue as a result of more taken from the Polity IV database.

effective and efficient tax authorities.

From the regression analysis using panel

6. Decision to Adopt SARA logit and probit models, we find that government

effectiveness factors have a significant impact to

the SARA at the level of 90 % (see Table 6). Any

A question, then raises: why not all countries

increase in the value of government effectiveness

adopt the SARA model when it is thought to be more

by 1 point will drive the decision to adopt

superior? There is no exact answer theoritically

SARA possibilities between 0.11 to 0.40 points,

and empirically. Therefore, we tried to do a binary

considering other factors constant. In other words,

choice regression models to reinforce what criteria

SARA will tend to be adopted in countries that

that can provide better answer for a country’s

have better government effectiveness. Government

decision to adopt SARA. 23

effectiveness variable indicates captures

perceptions of the quality of public services, the

The adoption of SARA is not solely influenced

quality of the civil service and the degree of its

by economic considerations but also take into

24

account political and institutional factors. Or independence from political pressures, the quality

of policy formulation and implementation, and the

in other words, countries only choose SARA if

credibility of the government’s commitment to such

there are condusive and supporting political and

25

policies. In addition, this variable also indicates

economic environments. To include variables

the quality of policy making and implementation,

related to political and institutional structure, we

as well as the government’s commitment to policies

23 Binary choice regression with institutional model of tax authority

(SARA=1, non-SARA=0) as dependent variable.

24 Maureen Kidd dan William Crandall, “Revenue Authorities: Issues and 25 Details on the description on governance indicator could

Problems in Evaluating Their Success”, IMF Working Paper WP/06/240, be access: http://info.worldbank.org/governance/wgi/index.

2006. aspx?fileName=wgidataset.xlsx#doc.